Get Approved for Florida Used Motor Vehicle Dealer Surety Bond

Frequently Asked Questions

Can I get a Florida dealership bond with bad or low credit?

Florida used motor vehicle dealer bonds are based on the credit of the owners and their spouses. What happens if everyone’s credit history isn’t perfect? Usually this means that the standard carriers will decline to offer the bond. We counteract that by working with a program with access to many surety carriers that do not necessarily follow the standard format. This means most dealerships will receive approval for a bond. Obviously, every case is different, and in some cases, there isn’t a carrier that is willing to approve, but in most cases, options can be provided.

How much does a Florida used auto dealer bond cost with bad or low credit?

This is different for every business. It can be as low as $250 or as high as $3,000. Depending on the specifics, number of owners, financials of the business, and just exactly what the credit of the owners and their spouses is.

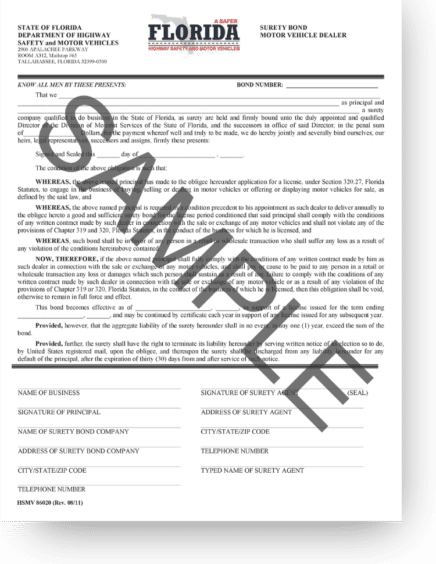

What is a Florida Used Motor Vehicle Dealer Bond?

A Florida used motor vehicle dealer bond is a surety bond required to get your used dealer license. The bond guarantees payment to the state if the dealership violates specific laws and rules regarding the sale of a used auto.

Who is required to purchase a used automobile motor vehicle surety bond?

All independent used auto dealerships are required to have a surety bond for $25,000 (also known as Florida Used Auto Dealer Motor Vehicle Bond) or an irrevocable letter of credit in the amount of $25,000.

Why do I have to buy a used automobile motor vehicle surety bond?

The purpose of the bond is to guarantee payment up to the bond limit for the financial loss caused by breaches of sales contracts and/or state regulations as written into the Florida Statutes 319 and 320. The Florida Department of Highway Safety and Motor Vehicles requires proof of bond form 86020 when obtaining or renewing your used automobile dealer license. This is necessary for both retail and wholesale dealerships.

Are surety bonds insurance?

Motor vehicle dealer bonds are not insurance. They are a guarantee of payment through an insurance company. This means that if a bond has to pay a loss the bonding company (also known as surety) will require reimbursement from the bond purchaser (also known as the principal). More simply stated, you have to pay the insurance company back for any losses they pay out on behalf of the bond.

What impacts the cost of your bond?

Used automobile motor vehicle dealer bonds are based on the ability of the principal (entity or person named on the bond) to repay the surety (the insurance company) in any situation where the bond has had to pay a loss. For this reason, the financial credit of the business, business owners, and sometimes even their spouses can all affect the cost of the bond. It’s important to note that it’s not just your credit score that insurance companies look at but also the ability of the principal to pay the bond back in a one lump sum or very short period of time. That is because, unlike a line of credit or a mortgage, there are no or extremely limited payment options to repay the loss paid by the surety. Check out our blog for more information about surety bonds.

Can Florida Used Motor Vehicle Bonds be canceled?

Under most circumstances, yes. If your business closes and you need to cancel the bond, you can request a cancellation from the carrier. Additionally, if your bond is with a higher-risk program with premiums paid in installments, the bond will be canceled if an installment payment is not received on the due date.

What if I am declined for the bond?

Because Florida Used Auto Dealer Bonds are based on the credit of the owners and their spouses, there are times that the credit history causes a carrier to decline writing the risk. We work with several bonding companies that may consider the higher-risk bonds in a situation like that. The bond premiums for these situations are generally higher than the standard program.

What happens if the insurance company pays a claim but my business / dealership is closed?

The used auto dealer bond application requires that the corporation pay back the premium and requires the owners to indemnify the insurance company personally. This means that even if the business is closed, the owners will still personally owe the money paid due to a claim back to the insurance company.